The correction in stock prices may be gathering steam, and the potential for a full-blown liquidity crisis seems to be rising. The reason may be that several big players in commercial real estate have recently defaulted on billions of dollars’ worth of loans.

Last week, in this space I wrote: “Something happened to the markets around Valentine’s Day which could reverse the recent uptrend.” Well, the trend is increasingly wobbly, and we are getting new information which may explain at least part of what’s happening.

Real Trouble in Real Estate

The hotter than expected PCE (Personal Consumption Deflator) data grabbed the headlines. But it seems that its arrival on the scene may be more of a catalyst for an already churning dynamic in the market than the cause for the renewed selling on 2/24/23.

Think commercial real estate defaults.

Over the last few weeks, in this space, I’ve reported that several major real estate investors have faced increasing difficulties. I’ve also noted that it is possible that these, along with other commercial property REITs that are having problems with foreclosures, may have been selling U.S. Treasury bonds in order to raise cash to fund operations as their cash flow dries up due to rising vacancies.

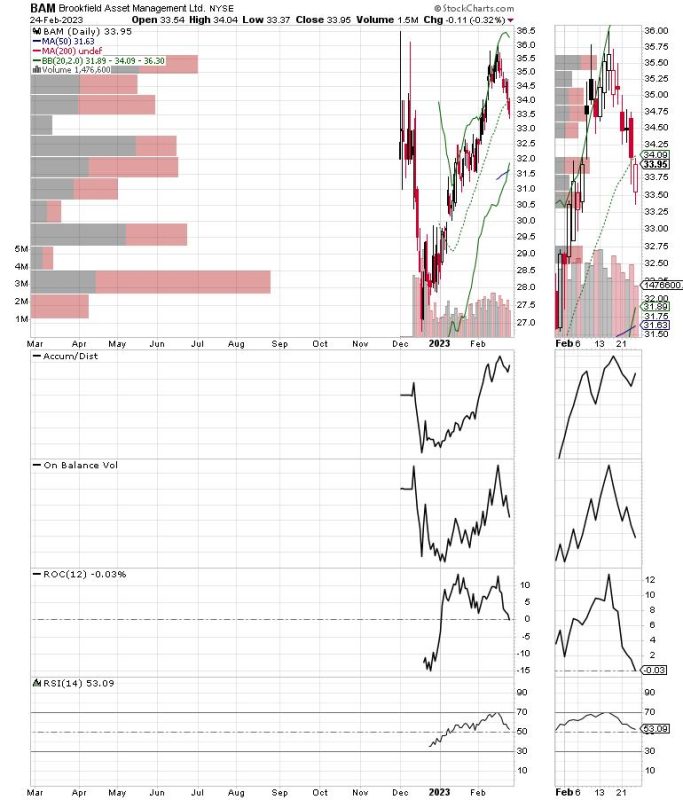

I’ve noted that Brookfield’s LA default (highlighted in prior link) has been well reported, while the even bigger Blackstone (BSX) is also having its share of problems along with Starwood (STWD). Brookfield’s (BAM) CEO Bruce Flatt is calling the L.A. default insignificant, while citing demand for premium space around the world, in places like Dubai, as more than enough to offset the L.A. issues for the company.

Nevertheless, the Toronto-based asset manager’s stock is rolling over along with the market for sure.

If there is a worsening of the situation the default, which we may look back upon as the one that broke the camel’s back, is that of Pimco’s $1.7 billion worth of mortgage notes tied to buildings owned by Pimco’s Columbia Property Trust in Los Angeles, Boston, New York and Jersey City, New Jersey.

Together, Pimco and Brookfield have defaulted on nearly $2.5 billion. But there seem to be more on the way, as The Real Deal.com website recently reported the Chetrit Group just defaulted on an $85 million loan in the tony New York City Hudson Yards property. If things don’t improve soon, and margin calls escalate, we could see a complete reversal of the recent rally in stocks.

Just in case, I’ve just added some new select hedges to my model portfolios. You can check them out here with a free trial to my service.

Bond Yields Test Crucial Resistance Levels as Liquidity Woes Continue. REITs are Heading Lower.

As I noted, above the commercial real estate market is facing serious headwinds. Moreover, if things don’t improve fairly quickly, the problems could spread to other areas of the market.

Meanwhile, the U.S. Ten Year note yield (TNX) has stubbornly remained above 3.8% and seems to be mounting an attack on the 4% area. This may be in response to selling by investors, who are having trouble making payments due to an increasingly restrictive Federal Reserve. A move above 4% would be a major negative for stocks, which could trigger very aggressive selling.

The rise in treasury bond yields has spawned a major reversal in mortgage rates, which is likely to dampen or at least slow the potential bottoming of the residential real estate market.

The homebuilder sector (SPHB) has been fairly steady in comparison to other areas of the stock market, but a move above 4% on TNX could send mortgage rates to levels near or above 7%. If that happens, it is likely to kill the housing market. Already, the homebuilder sector (SPHB) is threatening to break below its 50-day moving average.

Even more dire is the situation in commercial real estate, where the Dow Jones Real Estate Index (DJR) has just broken below its 50- and 200-day moving averages and could be headed significantly lower if there is no improvement in the market’s liquidity. Note the close inverse relationship between TNX and DJR and how they both reflect on the S&P 500 (SPX).

For a detailed explanation of how to manage your portfolio during a liquidity crisis, watch this Your Daily Five video.

Test of Key Market Support is Unfolding

The New York Stock Exchange Advance Decline line (NYAD) broke below support at its 20-day moving average last week and is now on its way to a test of its 50-day moving average.

Meanwhile, the S&P 500 (SPX) easily sliced through the 4000 area and is now actively testing the key support band of 3950 and the 200-day moving average.

The Nasdaq 100 Index (NDX) broke below the 12,200 and is now testing the support of the 200-day moving average.

For its part, the CBOE Volatility Index (VIX) is still lagging the current bearish trend due to a larger focus by option traders on contracts which expire in short periods of time, while VIX measures the volatility of longer-term options. Still, VIX is showing signs that it wants to turn up in a hurry.

When VIX rises, stocks tend to fall, as rising put volume is a sign that market makers are selling stock index futures in order to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying, and it eventually leads to call buying. This causes market makers to hedge by buying stock index futures, raising the odds of higher stock prices.

Liquidity tried to stabilize on 2/25/23, but the Eurodollar Index (XED) still closed below 95, which had been a reliable support level. Note the market’s most recent rally, off of the October bottom, has corresponded to this flattening out in liquidity. Note how the continuous decline in XED corresponded to the bear trend in 2022 and how the current liquidity reduction has impacted the market negatively.

You can learn more about how to gauge the market’s liquidity in this Your Daily Five video.

To get the latest up-to-date information on options trading, check out Options Trading for Dummies, now in its 4th Edition—Get Your Copy Now! Now also available in Audible audiobook format!

#1 New Release on Options Trading!

Good news! I’ve made my NYAD-Complexity – Chaos chart (featured on my YD5 videos) and a few other favorites public. You can find them here.

Joe Duarte

In The Money Options

Joe Duarte is a former money manager, an active trader, and a widely recognized independent stock market analyst since 1987. He is author of eight investment books, including the best-selling Trading Options for Dummies, rated a TOP Options Book for 2018 by Benzinga.com and now in its third edition, plus The Everything Investing in Your 20s and 30s Book and six other trading books.

The Everything Investing in Your 20s and 30s Book is available at Amazon and Barnes and Noble. It has also been recommended as a Washington Post Color of Money Book of the Month.

To receive Joe’s exclusive stock, option and ETF recommendations, in your mailbox every week visit https://joeduarteinthemoneyoptions.com/secure/order_email.asp.